The Future of Luxury in 2026: The End of Automatic Luxury

Luxury is not disappearing. It is losing a form of ease.

I do not believe in “the end of luxury.” The phrase feels too simple, almost too convenient. What is disappearing, however, is a certain ease: the kind of luxury that could rely on China, tourism, price increases, the power of the logo and the historical aura of major houses to mechanically generate desire. In 2025, Bain & Altagamma estimate that the global luxury market remains broadly stable at around €1.44 trillion, but that personal luxury goods are declining, while consumers increasingly turn toward experiences rather than ownership. The signal is clear: luxury is not dying. It is becoming harder to earn. (Bain & Company)

“Luxury is not dying. It is simply becoming harder to earn.”

Major groups are entering a phase of discipline

The weak signals are piling up. LVMH is selling Marc Jacobs to WHP Global after having already sold Off-White. Kering is placing Gucci at the center of a deep turnaround, with a renewed focus on product offer, distribution and client engagement. Burberry is returning to its fundamentals through Burberry Forward, while its 2024/25 revenue fell to £2.461 billion and adjusted operating profit dropped to £26 million. These are not just financial adjustments. They are signs of an industry becoming more selective, almost Darwinian: a brand can no longer rely on being known, expensive or heritage-driven. It has to prove why it still matters. (WWD)

Luxury’s problem is not being expensive

Luxury has never been afraid of price. Price is part of its language: it creates distance, tension, a boundary. But price becomes dangerous when it becomes more visible than desire. For several years, some houses were able to raise prices because the market could absorb it. Today, the client is looking more closely. They compare. They question the material, the service, the rhythm of collections, the boutique experience, the coherence of the story. A luxury brand can no longer simply say, “we are a house.” It has to make people feel that it still has a form of advance: in taste, in gesture, in the way it understands its time without chasing it.

Real rarity resists better than narrated rarity

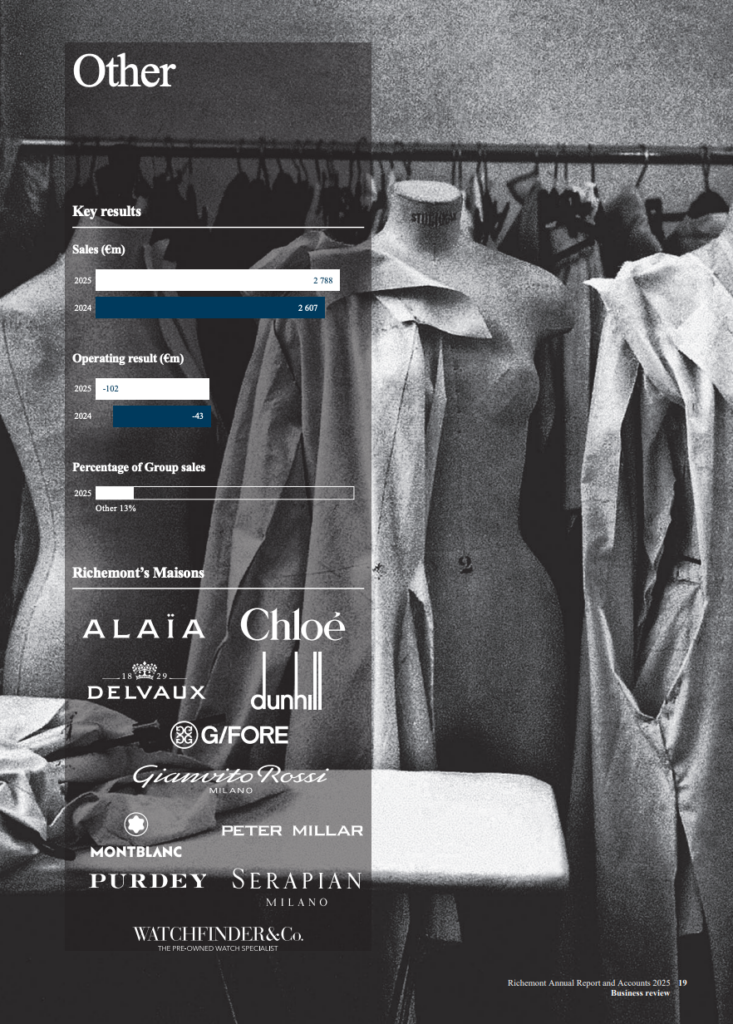

Not all brands are slowing down in the same way. Hermès reported €4.1 billion in revenue in the first quarter of 2026, up 6% at constant exchange rates. Richemont also shows a strong polarization: its jewellery maisons grew by 8% in 2025, while its specialist watchmakers declined by 13%. This contrast tells us something essential: the luxury that holds is often the one built on structural rarity, real product depth and a patient client relationship. The more vulnerable luxury is the one that has expanded its offer too widely, overexposed its imagery, or stretched its pricing too far. (Hermès)

Alo Yoga and the temptation of a more experiential luxury

Alo Yoga is not a European luxury house, and it would be clumsy to mix categories too quickly. But its activation on a 72-meter private yacht in Cannes, with Alo Voyage: Wellness Club at Sea, says something very accurate about the moment. Status is no longer expressed only through the object one owns. It also moves through the body one maintains, the places one accesses, the rituals one adopts, and the way one gives an aesthetic form to one’s life. This may be where a form of “Californication” of luxury begins to appear: less heritage distance, more body, wellness, light, movement and community. It is not the same luxury, but it is a signal that historical houses would be wrong to dismiss. (FashionNetwork)

The future of luxury will no longer be only European

Paris, Milan, Geneva and Florence remain immense symbolic capitals. But they are no longer alone. Brands from the Gulf, the Middle East and Asia no longer want to simply consume European luxury; they want to write their own version of luxury. The trap would be to copy Europe: fake heritage, marble, gold, French vocabulary, artificial storytelling. That will not be enough. The most interesting brands emerging from these regions will have to translate something deeper: a relationship to hospitality, fragrance, care, ceremony, gifting and time. A brand does not become global by erasing its origin. It becomes global when its origin becomes legible, desirable and shareable.

Conclusion: luxury must become necessary again

The real question for 2026 is not: “will luxury survive?” The real question is: “which brands still deserve to be desired?” Visibility is no longer enough. Being posted, commented on, activated or launched is no longer enough. The brands that will win in the coming years are the ones that will create less noise and more necessity; the ones that will align product, service, image, experience, culture and distribution with a new level of precision. Luxury is not dead. It is simply becoming more demanding. And for the brands willing to accept that level of discipline, this period is not a crisis. It may be the most interesting strategic opportunity in years.